by Dr. Hou Zhenhai

Straits Financial (China) Chief Strategist

|

Abstracts:

|

|

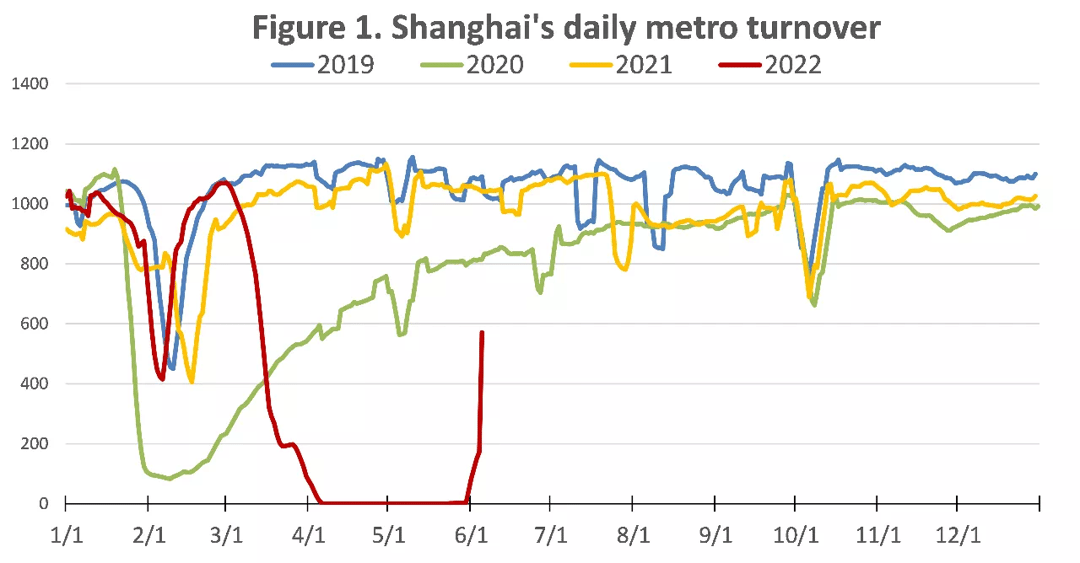

I. The end of lockdown and hope of more pro-growth policies drive a market risk-on rally. Since May, although the impact of Omicron on China’s economy has continued to increase, the voice calling for more pro-growth policies has also been increasing. In particular, the National State Council’s teleconference on stabilizing the macro economy held on May 25 greatly boosted the market’s confidence in future economic recovery and policy support. At the same time, the two core cities of Beijing and Shanghai, where the domestic Omicron infections are most serious and which have the greatest impact on China’s economy, have gradually lifted the lockdown after June 1st. From a policy perspective, the speed to end lockdown and restore outdoor work is quicker than expected. For example, we saw that on Monday, June 6, the Shanghai metro turnover reached 5.71 million people, which is already close to about 50% of the normal level (Figure 1). At the same time, most of Shanghai’s consumption venues, including supermarkets, restaurants, and other places with relatively dense crowds, have also resumed operations. Therefore, the market expects that the government seems to be more inclined to “maintain growth” now in the balance between the two policy goals of “strictly dynamic infection controlling” and “maintaining growth”. |

|

|

Source: Bloomberg, CEIC, Wind |

|

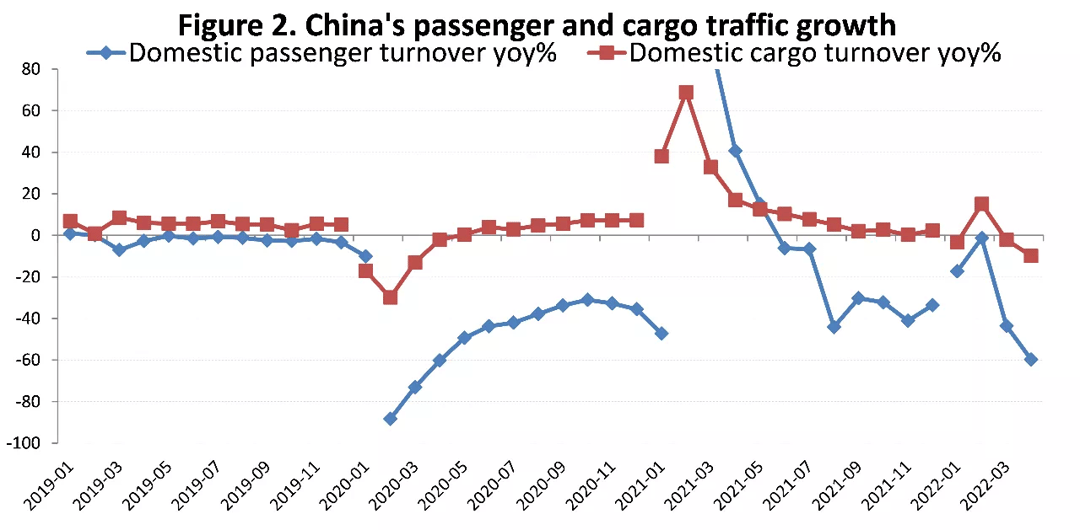

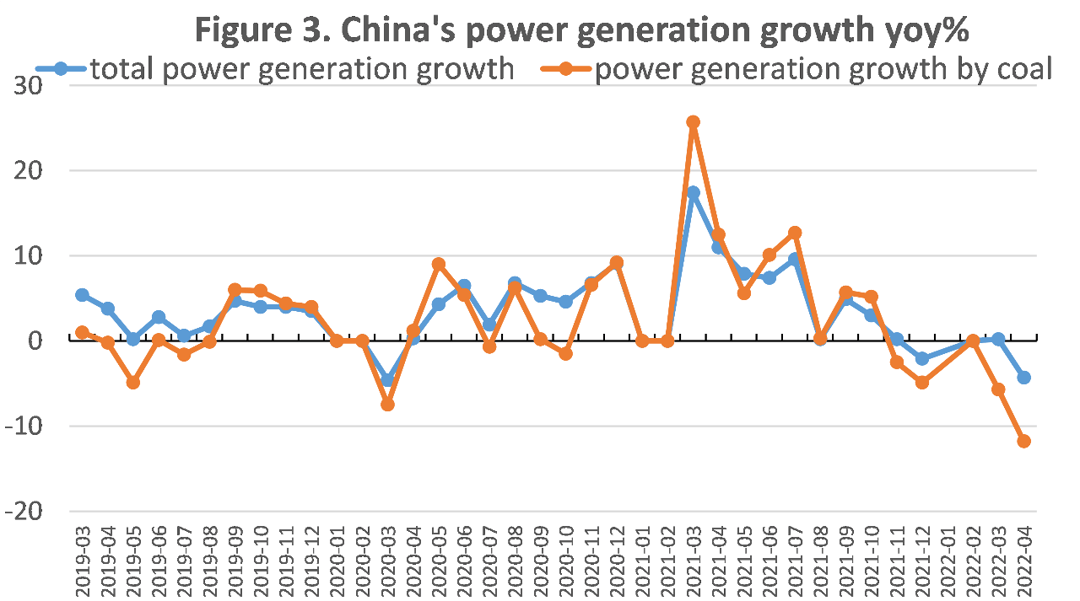

Premier Li Keqiang also stated that he will strive to resume work and production in June to ensure that domestic GDP does not experience negative growth in Q2. And we know that due to the impact of Omicron in the two months of April and May, the economic losses and impact caused are no less than that of the Wuhan pandemic in early 2020, while China’s GDP growth rate in the Q1 of 2020 was -6.9%, and in 1H of 2020 GDP growth was -1.7%. However, it is quite difficult to restore the GDP growth rate in Q2 to positive territory just by the growth in June. For example, we can see that it is most closely related to economic growth, and it is also several major indicators in the so-called “Keqiang Index”, including passenger traffic, cargo traffic and power generation. Passenger and cargo traffic in April was -59.7% and -9.9% YoY respectively (Figure 2). Although the data for May has not been released, it is expected that the improvement from April will be very limited. The year-on-year -4.3% year-on-year power generation in April is consistent with the lowest growth rate in March 2020 (Figure 3). |

|

|

Source: Bloomberg, CEIC, Wind |

|

|

Source: Bloomberg, CEIC, Wind |

|

On the one hand, it is extremely difficult to ensure positive GDP growth in Q2, but from another perspective, this also leads the market to expect that more and larger “strong stimulus” measures may still be on the way, besides just unlocking and work resumption. Because otherwise, reaching positive growth in Q2 or growth target for the whole year (such as around 5%) will be impossible.

Therefore, we believe that throughout June, the market may be full of expectations for strong policies to “maintain growth”, i.e. the first is “credit loosening”, that is, promoting bank credit and government bond issuance to increase investment growth. The next step may be a “further ease of fiscal policy” to stabilize employment and household consumption by reducing taxes and increasing subsidies or stimulus.

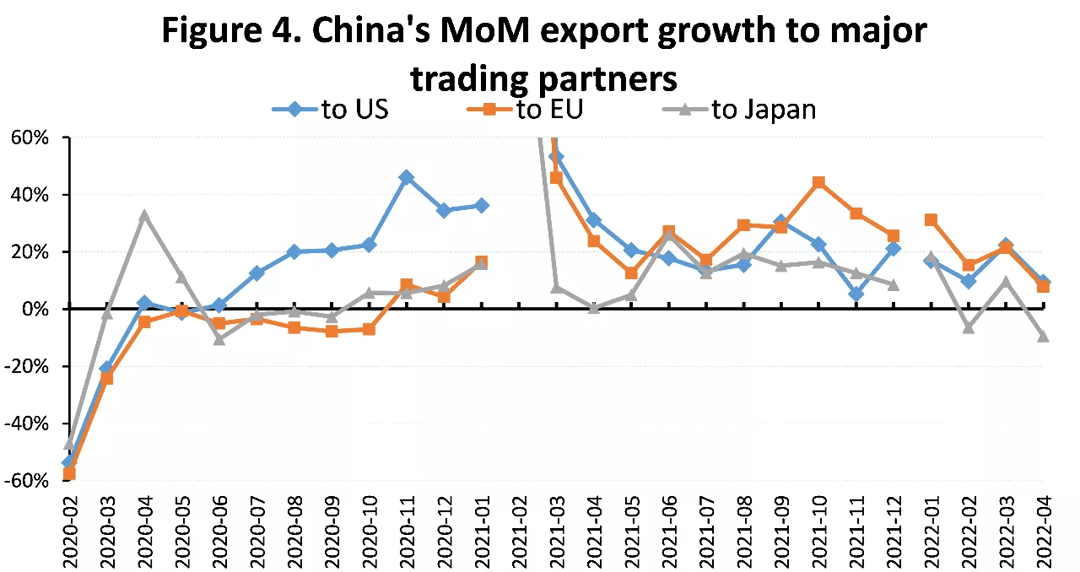

II. The Chinese economy will still need more stimulus. Although market expectations are relatively strong, we believe that the current policy efforts are still insufficient to reverse the downward pressure on the economy. At the same time, this year’s pandemic mainly affected economic activities from March to May, which is the traditional peak season for consumption and production in China. This was different from 2020 when the pandemic mainly occurred in the off-season of consumption and production around the Spring Festival from February to March. Secondly, the recovery of China’s economy in late 2020 was not only the result of domestic policy stimulus but also largely benefited from the spread of the overseas Covid-19 pandemic and the large-scale fiscal and monetary stimulus in the EU and the US, resulting in the shift of large-scale production and consumption demand to China’s exports. In 2020, after the downturn in Q1, China’s exports rebounded rapidly, especially in H2 of the year, the growth rate reached a historical peak, especially the growth rate of exports to the US was as high as 40%. This year, the situation is completely different. Countries in the EU and the US have entered a cycle of fiscal cliffs and monetary tightening. At the same time, as Omicron impacts in other producing countries in the EU, America and Southeast Asia have abated, production has been quickly picked up and orders have begun to flow back to these countries, and the growth rate of China’s exports in 2022 will face continued downward pressure (Figure 4). |

|

|

Source: Bloomberg, CEIC, Wind |

|

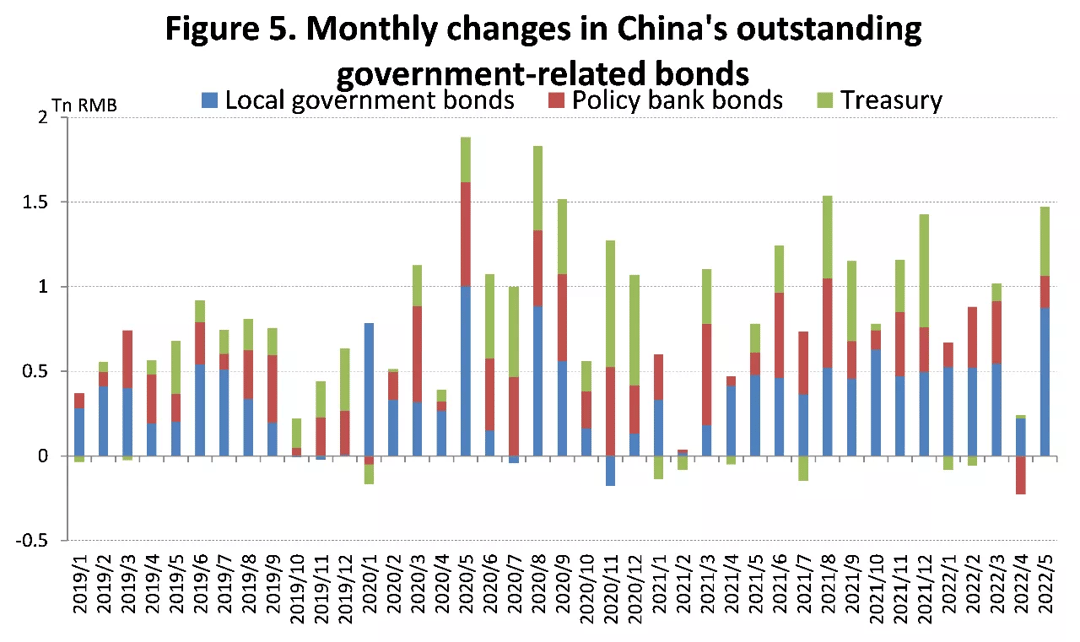

Taking the above factors into consideration, it can be said that in H2 of this year, a stronger stimulus policy than in 2020 is needed to make it possible for the domestic economy to recover. At present, the main force of domestic policy is still to stabilize investment by increasing government bond issuance, while trying to stabilize the property market through policies including interest rate cuts and relaxation of purchase restrictions. These methods were also usually adopted every time in the past 10 years when China’s economic growth encountered great downward pressure. We saw an increase in government bond issuance in May, resulting in net government bond financing of nearly 1.5 trillion RMB (Figure 5). |

|

|

Source: Bloomberg, CEIC, Wind |

|

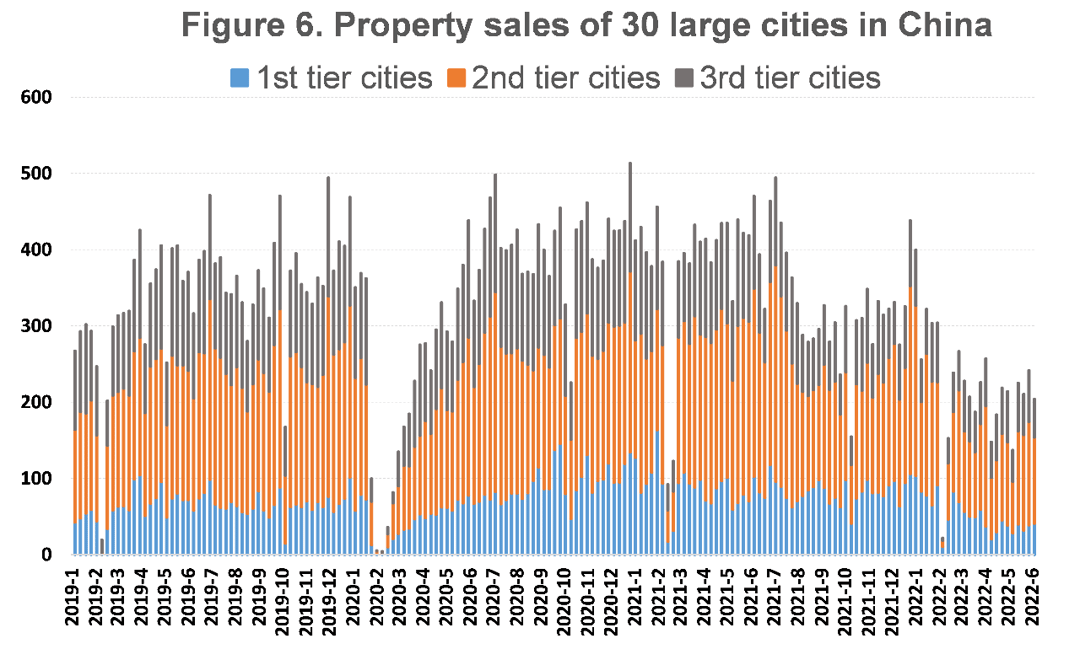

However, compared with the beginning of 2020, such government bond issuance is still not enough to ensure growth. At the same time, we also see that, in addition to government bond issuance, the current corporate financing demand and residents’ housing loan demand are very sluggish, and those demands may not have a significant improvement in the next few months, so we still need to pay close attention to whether the future policy will be implemented to stimulate loan demands. In particular, for the past stimulus policies to play a sufficient role in stabilizing economic growth, to a large extent, households need to leverage up and increase their property purchases. At present, there are no stimulus policies similar to the “township rebuilding” and “old town renovation” policies in the past, which gave money directly to the household sector. It is doubtful whether Chinese households can continue to buy more properties just by leveraging up. So far, the high-frequency data on property sales is still very sluggish (Figure 6). |

|

|

Source: Bloomberg, CEIC, Wind |

|

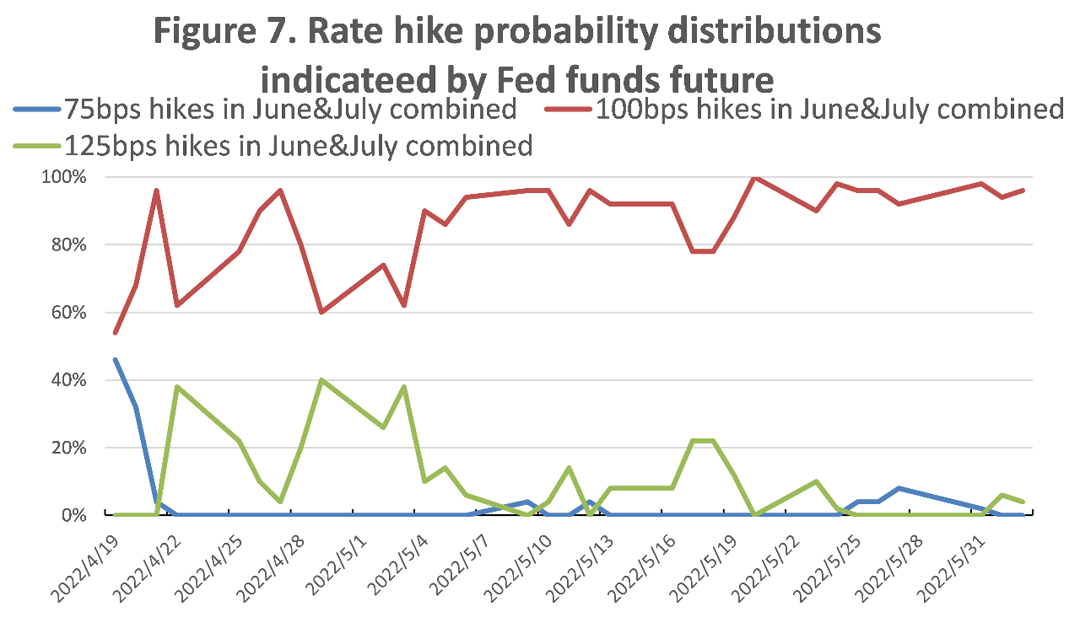

III. Market rebound opportunities and risks The A-share market has rebounded from its bottom for more than a month now. From the perspective of stock indexes, the rebound has recovered about 30-40% of the previous largest decline. Therefore, we believe that there is not much room for a rebound in the near term, and the opportunities and risks to judge whether the market can further rise in the future mainly depends on 1. The introduction and implementation of specific stimulus policies; 2. The risk of Omicron relapse and its policy constraints; 3. Real economic data and corporate earnings recovery. Regarding the specific stimulus policies, the first thing we need to see is the rebound of social financing in May and June. The May 25’s State Council teleconference on stabilizing the macroeconomy emphasized the important role of investment. Therefore, the theoretical minimum new social financing in May and June should exceed 3 trillion and 4 trillion respectively. Otherwise, the market will have doubts about whether the economy can resume growth. Secondly, with the acceleration of work resumption and unlock, small-scale Omicron infections may inevitably reappear in some areas. Therefore, there are still large uncertainties in whether the pandemic will become an important constraint over economic recovery again. And this is one of the major risks we think the market may face in the next month. In addition, the Federal Reserve will hold two FOMC meetings in June and July. The market expects that each meeting the Fed will raise interest rates by 50bps respectively, which means that by the end of July, the US federal funds target rate will rapidly increase by 100bps to 1.75~2%. This may also be the period the market sees the fastest short-end rate increases in this round of the rate hike cycle. At the same time, during this period, major overseas central banks, including the ECB, the Bank of England, and the Australian Central Bank, are likely to raise interest rates together, which is very different from the global environment in which China has sharply cut interest rates and eased after the end of the Wuhan pandemic in 2020. |

|

|

Source: Bloomberg, CEIC, Wind |

|

Finally, the market will pay more attention to the effect of the actual economic recovery and the degree of corporate earnings recovery in Q3. Therefore, the impact of economic indicators more closely related to the real economy, including property sales, automobile sales, traffic and electricity generation, will further increase. Therefore, we can think that before the end of June, the dominant logic of the market rebound will still be the expectation of policy stimulus and the recovery of pessimistic expectations. In July, the market will shift to pay more attention to the performance of the real economy and the actual implementation of stimulus policies. IV. Market strategy We believe that the market’s recovery from pessimistic expectations is about to come to an end, and the A-share market has also entered a previously intensive trading area. Therefore, there may be some volatility in the short-term market, but the overall downside risk is not limited in our view. After the market stabilizes, whether it can further push the index to rise will depend to a greater extent on the implementation of actual stimulus policies in the future, as well as how to balance the contradiction between “dynamic infection control” and “maintaining growth”. Therefore, incremental social financing, new infection data, changes in lockdown and restrictive policies, and specific industry support and stimulus policies will largely determine the trend of A-shares before the end of June. After July, the market will pay more attention to the actual effect of economic recovery and the level of restoration of business conditions. For US stocks, we are currently in a relatively neutral judgment. On the one hand, the rate of interest rate hikes and QT by the Fed will be significantly accelerated shortly, and at the same time, commodity prices represented by oil prices will remain high. Therefore, we believe that overseas stock markets will still find it difficult to see a major turnaround. But from another perspective, the relatively pessimistic sentiment in the short-term market has peaked, while the market’s expectations for long-term inflation have declined a little bit, which are also positive factors that will help stabilise US stocks in the short term. Therefore, our current attitude towards US stocks tends to be neutral. We believe that the trend of domestic commodities is highly correlated with A shares in the near term because the logic behind them is similar. Driven by the State Council’s teleconference on stabilizing the macro-economy, the commodity market’s rise has also benefited from the improvement in expectations. This is shown by the fact that the rise in commodity futures recently is much larger than that of physical prices, and some products have changed from the previous future-physical discount to premium, indicating a reversal in market sentiment. But for most commodity investors, it may be difficult to judge macro sentiment. Therefore, the trend of A-shares can be considered an indicator of short-term macro sentiment. Therefore, we believe that the trend of short-term domestic commodities will be more consistent with that of A-shares. On one hand, overseas commodities are affected by insufficient supply, and on the other hand, they are also affected by the Fed’s interest rate hike and the US dollar strength, and the trend may be more differentiated. In the short term, we are still optimistic about crude oil and agricultural products. In July, we may further analyze the opportunities for overseas non-ferrous metals and other products based on the actual implementation of China’s stimulus policies. |